This method can only be used when the investor possesses effective control of a subsidiary which often assumes the investor owns at least 501. It is considerably easier to account for investments under the cost method than the equity method given that the cost method only requires initial recordation and a periodic examination for impairment.

accounting entry for investment in subsidiary

accounting entry for investment in subsidiary is a summary of the best information with HD images sourced from all the most popular websites in the world. You can access all contents by clicking the download button. If want a higher resolution you can find it on Google Images.

Note: Copyright of all images in accounting entry for investment in subsidiary content depends on the source site. We hope you do not use it for commercial purposes.

Dividend received by the holding company from its subsidiary out of pre acquisition profits is treated as capital receipt.

Accounting entry for investment in subsidiary. The journal entry for its record being as follows. This has been treated as an investment in a subsidiary in the draft accounts at cost. How to account for subsidiaries.

A parent and a subsidiary must apply the same accounting policy. Other procedures are the same as associate to subsidiary. Subsequent to this the subsidiary company prepared accounts to 30 april 2016 which showed all assetsliabilities had been stripped out leaving solely the 100 issued share capital.

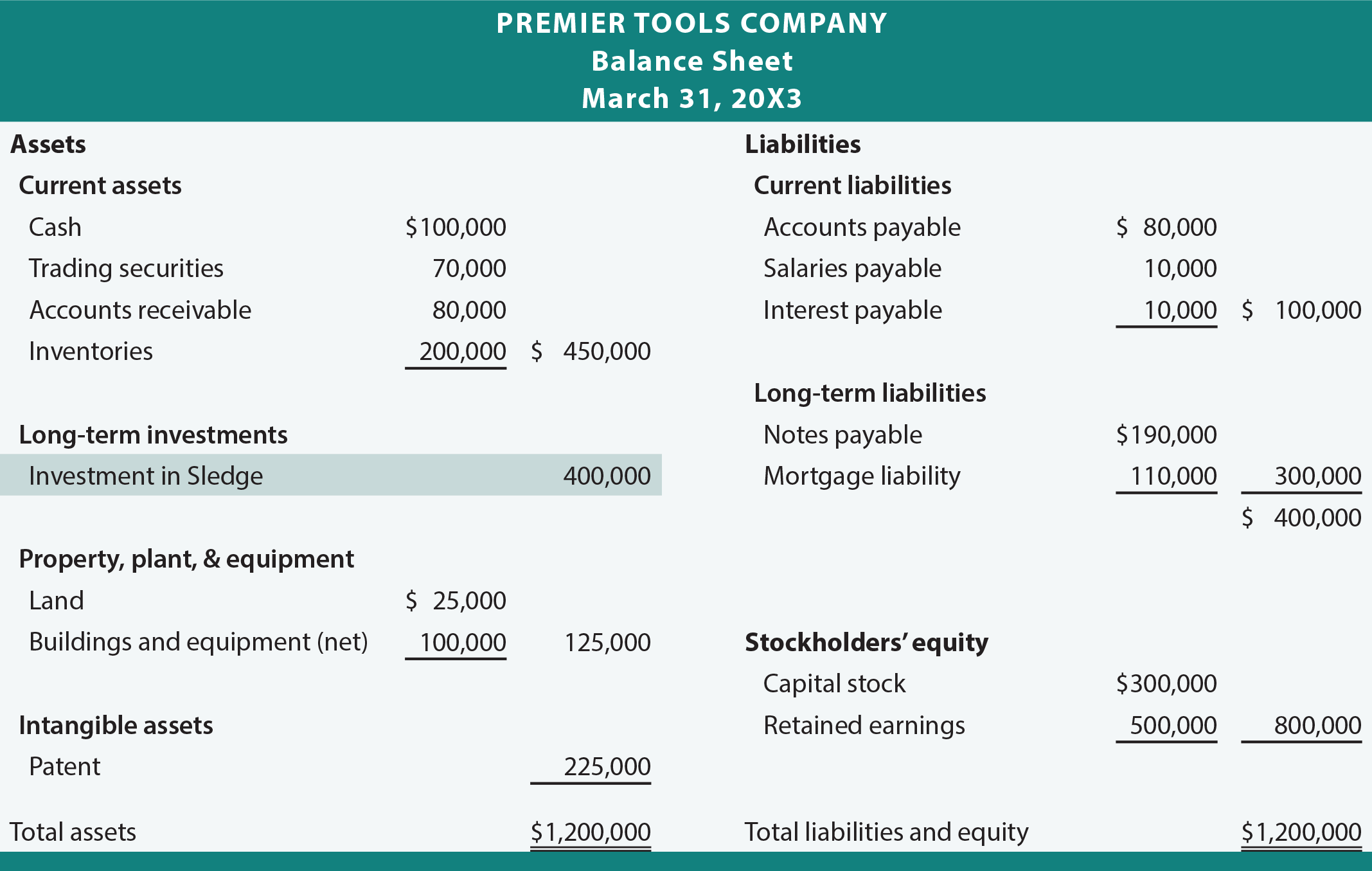

The consolidation method is a type of investment accounting used for consolidating the financial statements of majority ownership investments. The consideration was 400000. Debit your investment loss account by your share of the loss and credit your investment account by the same amount.

Your share of the loss reduces your investments accounting value and decreases your. A subsidiary is a company that is controlled by another company that owns 50 or more of its voting stock. Thanks for the detailed explanation kindly clarify how the gain on sale of investment in subsidiary will be reversed if we do a line by line consolidation.

By bryan keythman. The reason is that there is no investment in a subsidiary from the groups point of view all the time. The equity method is only used when the investor has significant influence over the investee.

The alternative method of accounting for an investment is the equity method. Equity method of accounting is used investment is initially recognised at cost and adjusted thereafter for the post acquisition change in the investors share of net assets of the investee. In this article we will discuss about the dividend from subsidiary company pre acquisition and post acquisition profits along with solved illustrations.

Ulike the consolidation method the terminology of parent and subsidiary are not used since the investor does not exert full control. The controlling company also called the parent company is said to have a controlling interest in. Equity method of accounting for investment journal entries.

Initially what would be the entry in subsidiary books and then at the time of consolidation. Instead the term investment is simply used. Will it amount to double accounting of gain in consolidated financials when we compute gain on loss of control in consolidated financial statements group books.

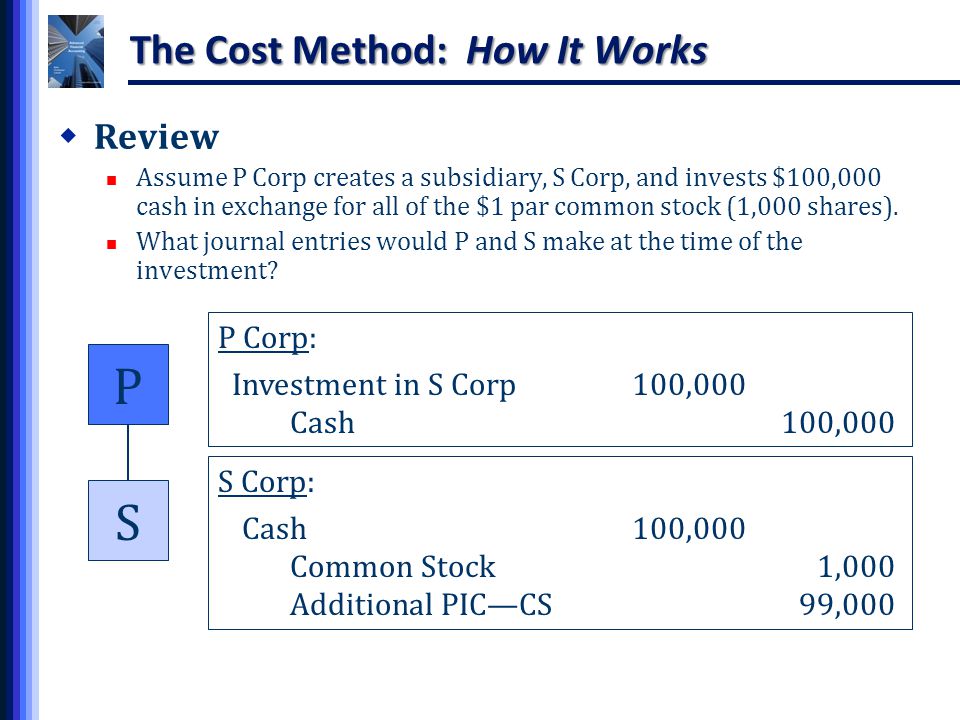

The journal entry is the opposite of the profit entry. The cost method is a type of accounting used for investments where the investor holds little to no influence over the investee.

Consolidation Accounting Facts Parent Co Paid 176 000 For